Table of Contents

The composition of investment instruments in a portfolio changes over time: some assets may grow quickly, while others may fall. Therefore, the equity holding may no longer align with the investor’s risk tolerance level and financial goals.

To fix this, it’s necessary to rebalance and restore the original asset allocation in your portfolio in line with your needs and overall strategy. Portfolio rebalancing is useful because it can help you earn more in the long run, but its main goal remains reducing risks.

Below we’ll look at why rebalancing matters, what it looks like, how often you should actually do it, and what to avoid to maintain profitability.

What Is Portfolio Rebalancing?

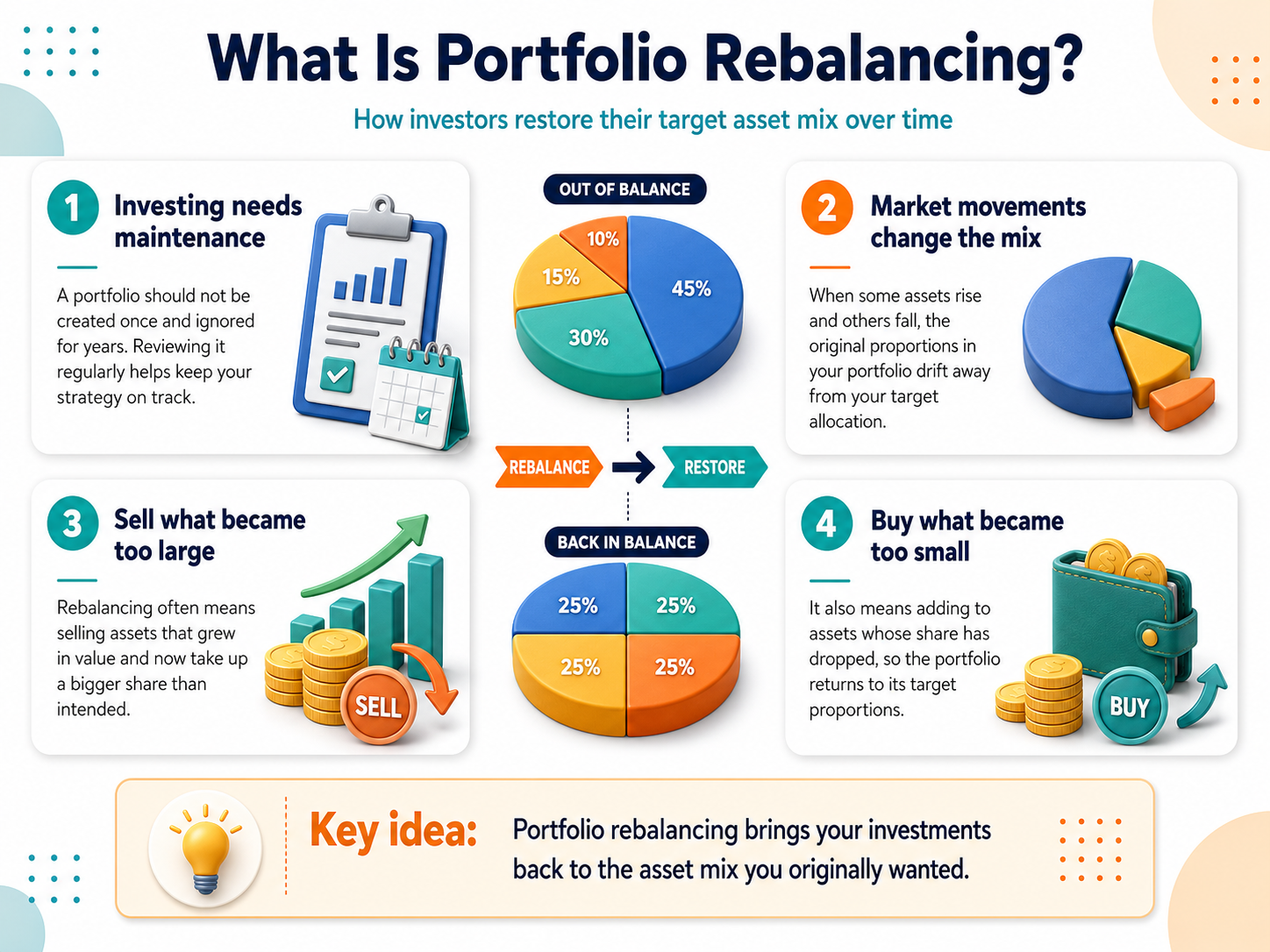

Investment management is an ongoing process that requires your involvement. It’s too risky to create a portfolio once and leave it alone for years. So, professionals recommend reviewing and adjusting it from time to time.

Portfolio rebalancing is the process of bringing a portfolio back to the target proportions of assets after market movements change the initial mix. In simple words, you’ll need to sell assets that have increased in value and taken up a larger share than intended and buy products whose share in your portfolio has decreased.

Here’s an example:

- You’ve built a balanced portfolio with 50% stocks, 30% bonds, and 20% cash.

- There has been a tech boom, and stocks of IT companies have skyrocketed in price. Now stocks make up 70% of your investments, constantly fluctuate, increase your risks, and make you nervous.

- You need to fix this by selling a portion of the overweight stocks, locking in profits, and distributing your money between the underweight bonds and cash. This way, you’ll return to the target allocation.

What Causes Portfolio Drift?

Portfolio drift happens because different assets move at different speeds, and market news can affect them unevenly. Volatile asset types like growth stocks and crypto tend to change value faster. Meanwhile, cash can slightly depreciate because of inflation. It’s normal, but if left unchecked, the holding may become riskier than you intended.

Why Does Portfolio Rebalancing Matter?

If a portfolio drifts, the investor’s risk exposure changes, often without them noticing it right away. It can get too aggressive when growth assets start taking over or too conservative when the share of stocks is going down.

Bringing the assets in the portfolio back to the initially set proportions you were comfortable with has several advantages:

- It helps you stick to your original plan and keep your investments under control. The portfolio structure will be intentional rather than accidental.

- It helps to maintain an optimal balance of risk and return and make the mix more aligned with your long-term goals.

- It helps you lock in gains and buy more relatively cheaper assets that have high growth potential. This may result in increased profitability.

- It encourages discipline, as it takes emotion out of investment decisions. Therefore, you are less likely to chase winners or panic-sell losers.

How Often Should You Rebalance Your Portfolio?

You may have heard that it’s recommended to review your investments every year or two. This is not the only appropriate strategy, though. There is also an option to rebalance only when allocations move too far from their targets. Let’s go through both methods so that you find one that is simple, consistent, and realistic for you to maintain over time.

Calendar-Based Rebalancing

The basic method includes reviewing the holdings at regular intervals. You’ll need to develop a fixed schedule and rebalance quarterly, semiannually, or annually. It’s worth putting reminders in your calendar so you don’t miss it. Calendar rebalancing is easy to understand and follow, so it’s attractive for beginners. However, the method has disadvantages. For example, it may lead to unnecessary trades if the portfolio has not changed much.

Threshold-Based Rebalancing

A calendar rebalancing approach might not work for you or even be detrimental, for example, if the market situation has changed dramatically. If you wait several months before the scheduled rebalancing, you’ll be missing out on opportunities to make money. So, the second method is to adjust asset allocation only when it moves far beyond a chosen limit.

With threshold-based rebalancing, you need to define the percentage deviation from the target value you can tolerate. This could be 5%, 10%, or 15%. As soon as the asset class deviates more than that, you should take action. This model is more responsive to the actual changes but also requires more monitoring and can feel a bit complicated.

To rebalance your portfolio efficiently, you don’t always have to perform large sell-offs. You can direct new contributions into underweighted assets, use dividends or incoming cash, or make smaller adjustments over time.

What Mistakes Should You Avoid?

There are the top 3 common mistakes that investors make when rebalancing a portfolio:

- Trying to rebalance as often as possible. Treating rebalancing like market timing can add extra costs and taxes, which can eat into returns, or force you to sell winners too early and buy assets just because of short-term price moves.

- Ignoring portfolio drift for too long. Rebalancing your portfolio works when you follow a simple plan. If you choose the calendar-based approach, stay consistent with the schedule. If you prefer a threshold-based option, react quickly to any significant deviations.

- Forgetting about taxes and costs. This is not a purely mechanical process with no real-world trade-offs. Every time you sell an asset, you pay a commission and then pay capital gains tax on the profit. So, consider this as well.

What Is the Best Portfolio Rebalancing Approach?

Rebalancing keeps holdings aligned with your goals and allows you to manage risk and emotion. It reduces the chance that one asset class becomes too dominant, supports discipline, and can help you increase profits in the long term by locking in gains and buying assets at a lower price.

Overall, the most effective strategy is one that the investor can understand, apply, and maintain. For many investors, a simple option, such as regular reviews, is sufficient. Others may prefer a more structured method with thresholds for greater control. Also, you can use both simultaneously. Choose the approach that best suits your needs.

Disclaimer: The content provided in this article is for educational and informational purposes only and should not be considered financial or investment advice. Interacting with blockchain, crypto assets, and Web3 applications involves risks, including the potential loss of funds. Venga encourages readers to conduct thorough research and understand the risks before engaging with any crypto assets or blockchain technologies. For more details, please refer to our terms of service.