Table of Contents

Active trading looks appealing at first. Fast decisions, real-time charts, the idea that the right call at the right moment could change everything. It's exciting. At least on paper.

The actual track record looks quite different. Cheaper, less stressful, and far less dependent on timing calls you're unlikely to get right – long-term investing across a diversified portfolio has outperformed active trading for most retail investors across most time periods. Not because it's exciting, but because it sidesteps a lot of the costly mistakes that short-term trading tends to invite.

This article breaks down why, without turning into a trader-versus-investor manifesto.

What Is the Difference Between Long-Term Investing and Active Trading?

Long-term investing is simple in principle. You buy shares, funds, or exchange-traded funds (ETFs) and hold them for years, sometimes decades. You're not trying to catch every move. You're betting that businesses grow over time and that staying in the market beats jumping in and out of it.

Active trading is a different approach. Traders buy and sell frequently, trying to profit from short-term price movements. Some trade daily. Others hold positions for a few days or weeks. The defining feature is that returns depend on getting timing right, consistently.

There's a related distinction worth knowing: passive versus active investing. Passive investing means tracking the market through index funds or ETFs with minimal decisions and minimal trading. Active investing, whether through a fund manager or by picking stocks yourself, involves trying to beat the market. Most of the time, long-term investing and passive investing end up in the same corner. But you can hold a handful of individual stocks for decades and that’s long-term investing too – just not passive.

Why Does Long-Term Investing Often Lead to Better Results?

It mostly comes down to compounding. But costs and badly timed decisions eat into returns more than most people expect.

Worth being clear, though. "Outperforms" doesn't mean long-term investing guarantees higher returns in every period. Markets fall. Patient investors face losses too. What it does mean is that, over most time horizons, the odds tend to be better.

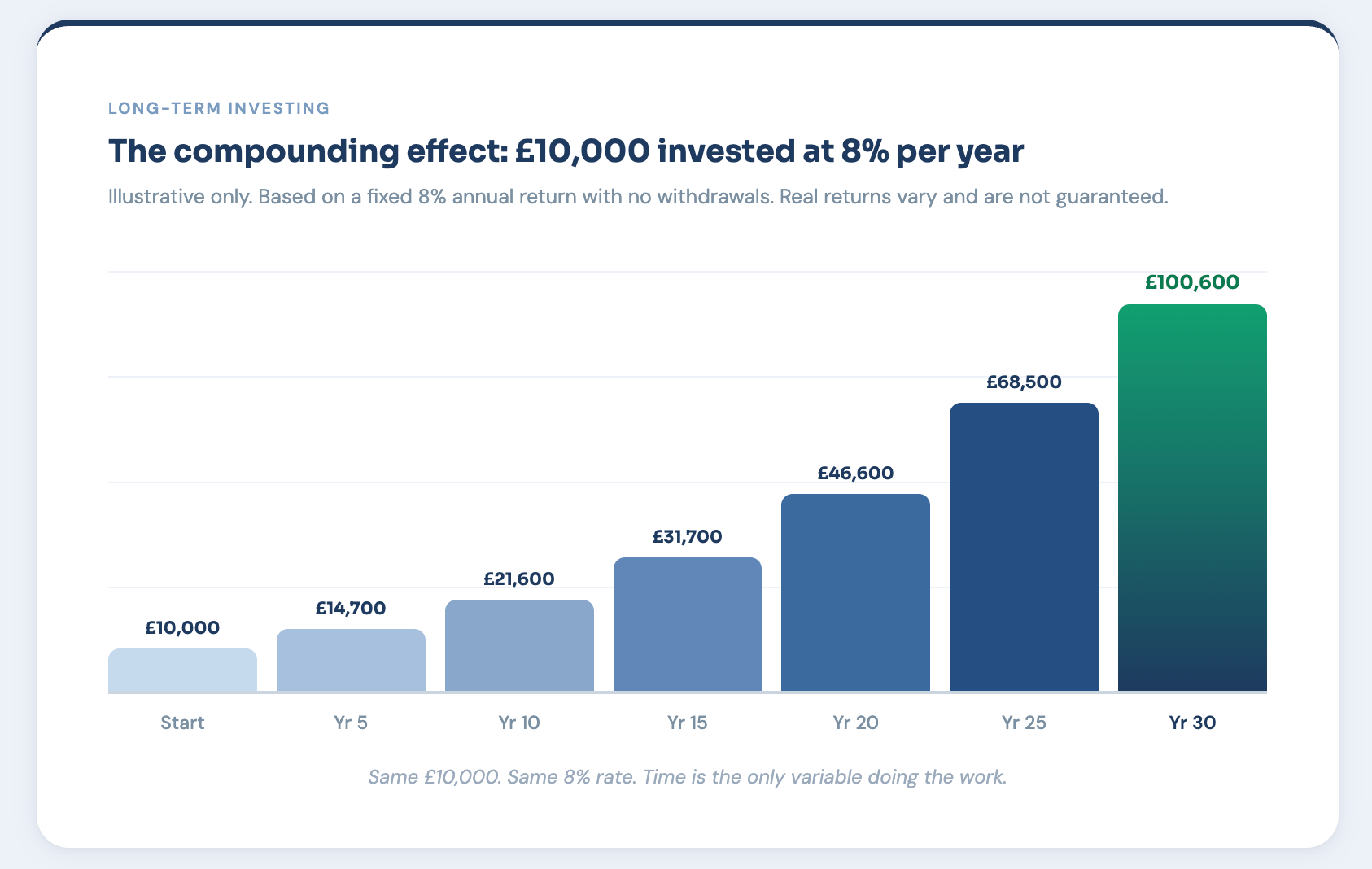

The Power of Compounding

Compounding is the process by which your gains start earning gains of their own. It’s slow to notice early on. A £10,000 stake growing at 8% a year reaches roughly £46,600 after 20 years and about £100,600 after 30. Same rate, same starting point. Time is the only variable that changes the outcome.

Active trading interrupts that process. Every time you sell, you reset the clock on compounding, trigger a tax event, pay a transaction cost, and need to decide what to buy next. Those interruptions compound against you.

Lower Costs and Less Friction

Every trade has a cost – a fee, a spread, sometimes both. In isolation these look small. Over hundreds of trades, they add up faster than most people expect.

Tax compounds the effect. In the UK, short-term capital gains (CGT) are taxed as income. Long-term investors who hold through a Stocks and Shares ISA, or simply hold for years before selling, often pay significantly less. That gap matters more than it looks when you run the numbers out over a decade.

Why Is Active Trading So Difficult to Sustain?

The appeal is understandable. Some traders do make consistent money. The statistics for most, though, are sobering.

Most retail traders lose money. Not as a rough generalisation, but as a finding that shows up consistently in broker data and academic studies. More surprisingly, the professionals don't fare much better. S&P Indices Versus Active (SPIVA) data puts roughly 80–90% of actively managed funds behind their benchmark over 15–20 year periods. The people paid full-time to beat the market, with institutional research and trading infrastructure, mostly can't do it consistently.

The problem is not just picking bad stocks. It's the full picture: transaction costs, taxes, the emotional pressure of watching positions move against you, and the near-impossibility of consistent timing. Miss just the ten best trading days in a 20-year market window and your returns roughly halve. Those ten days are impossible to predict in advance.

How Does Passive vs Active Investing Fit Into This Debate?

Passive investing means something specific: you buy a tracker fund, hold it, and don’t make active decisions about what to own.

The goal is to match the market at low cost, not beat it. Long-term investing can sit under that umbrella, or it can mean holding individual stocks for years – both qualify as long-term, but only the first is strictly passive.

Active trading is one version of a broader active approach. The overlap is the reliance on frequent decisions and the expectation of outperforming the market. In practice, both are harder than they look. And both carry a real chance of trailing behind an investor who does a buy and hold (i.e., simply bought a tracker fund and held it).

Does Long-Term Investing Carry Less Risk Than Active Trading?

Staying invested for the long haul doesn't mean avoiding losses. The 2007 crash, the March 2020 selloff, the dot-com collapse – anyone in the market through those periods lived through real drawdowns.

The type of risk is what changes, though. Timing risk – buying at a peak, selling in a panic – is where most long-term damage gets done. Staying invested longer reduces your exposure to exactly that kind of mistake.

The S&P 500 fell roughly 34% between February and March 2020. By August, it had recovered all of that. Investors who stayed in got their money back. Those who sold in March crystallised the loss and then faced a second judgement call – figuring out when to re-enter, under even more pressure than the first.

Who Is Long-Term Investing Best Suited For?

Realistically? Most people.

It suits beginners who are still learning how markets work. It suits busy professionals who don't have hours each day to monitor positions. It suits anyone whose main goal is steady wealth-building rather than market participation as an activity in itself.

Long-term investing rewards you for doing less. In most contexts, that would be a warning sign. In investing, it's actually one of the better things a strategy can offer.

Conclusion: Why Does Long-Term Investing Often Win Over Time?

Because the conditions that make it work – time, compounding, low costs, emotional steadiness – are available to almost anyone willing to wait.

Active trading is not impossible to do well. But it requires consistent skill, access to information, and a tolerance for pressure that most retail investors don't have available day to day. The odds are structurally against it.

The best strategy is rarely the most exciting one. It's usually the one an investor can stick to through the ups, the downs, and all the noise in between.

Disclaimer: The content provided in this article is for educational and informational purposes only and should not be considered financial or investment advice. Interacting with blockchain, crypto assets, and Web3 applications involves risks, including the potential loss of funds. Venga encourages readers to conduct thorough research and understand the risks before engaging with any crypto assets or blockchain technologies. For more details, please refer to our terms of service.