Table of Contents

Successful investors have one particular thing in common: The right portfolio. Building a portfolio that sets you successful will mean choosing the right assets for that portfolio. ETFs and Index funds are the heavyweights of the investing world, and for good reasons.

They are tools for building long-term wealth. In fact, most financial experts (and that one friend who actually seems to have their life together) will tell you that these are the smartest ways to get your money working for you.

In this piece, we are exploring what makes them look like twins yet act so differently which is one of the biggest confusions investors face in choosing how to build their portfolio.

What Is an ETF?

Exchange-Traded Fund (ETF) bridges traditional stock market and digital assets. It takes the best part of a mutual fund (owning a giant basket of different assets) and mixes it with the best part of a stock (the ability to buy and sell it whenever you want).

Instead of betting on just one company, you’re buying a tiny slice of hundreds of them at once, at fluctuating market prices throughout the day.

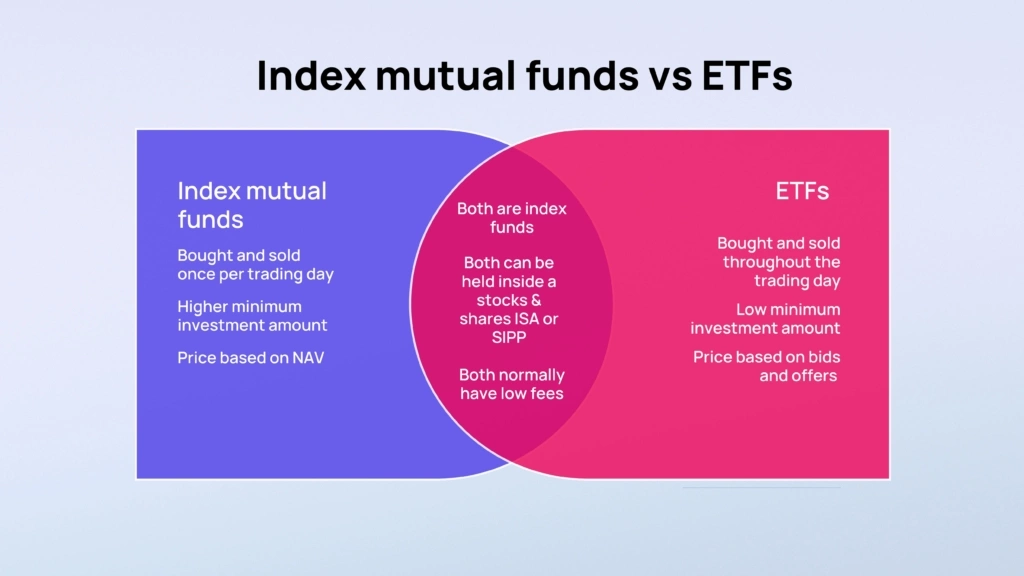

Since ETFs live on the stock exchange, they offer instant liquidity. You can buy or sell your shares in seconds at fluctuating market prices any time the doors are open. Whether it’s 10:00 AM or two minutes before the closing bell, you’re in control of the timing, not waiting for the end of the day.

Worried about honesty? You should be, but ETFs have a built-in BS detector called the creation and redemption mechanism. How does this work?

Behind the scenes, big institutional players are constantly swapping the actual assets for ETF shares and vice versa, which acts like a stabilizer. This ensures the price you see on your screen is an actual reflection of the real-time value of what’s inside the basket.

It’s a transparent setup for investors who want to know exactly what their portfolio is worth without waiting for a daily update. Simple, fair, and perfectly synced

What Is an Index Fund?

Index Funds are chill, disciplined marathon runners. An Index Fund is a type of mutual fund specifically designed to mirror the performance of a market index by using a passive investment strategy.

This passive management approach means you are not jumping from one price to another. Instead, you’re buying at the NAV (Net Asset Value), a price calculated just once a day after the market closes, ensuring everyone gets the same fair deal.

Index Funds are usually bought directly from the fund company skipping the middleman which makes them a hot deal for long-term accumulation. More like a set it and forget it process, you build wealth on autopilot.

ETF vs. Index Fund: The Showdown

You could own both an ETF and an Index fund that have exactly the same list of companies, yet your experiences as an investor will be totally different. It would be exact to say having identical twins with completely different behaviours.

While their DNA might be the same, their structural personalities are worlds apart. One is a social butterfly that loves the thrill of the exchange (ETF), while the other is a homebody that prefers the quiet discipline of a direct relationship with the fund company (Index Funds).

So even if they are similar, investors may have quite different experiences. It is therefore essential to choose the one that matches your financial frequency. Now let us look at their features:

Trading and Liquidity

Talking movements, ETFs are like fast paced auctions. They have intraday liquidity. This means you can buy and sell shares at fluctuating market prices any time of the day as soon as doors open.

On the flip side, an Index Fund presents its movements like a scheduled flight. It doesn't care about the opening show nor the midday party. It comes to the table at the end of the day at NAV (Net Asset Value). Everyone places their order at any time of the day and gets the price once the market closes.

While one gives the adrenaline of real time trading the other gives the comfort of a single, daily calculation.

Pricing Structure

The price tag on these funds puts the lamp light on their differences.

With an ETF, you’re dealing with Market Pricing. Since it’s out there mingling on the stock exchange, the price is constantly dancing based on supply, demand, and whatever the market is feeling at the moment. It is transparent yet with a catch- the bid-ask spread.

This means that you incur a small "convenience fee" for trading whenever you want. It's just the gap between the highest price a buyer will pay and the lowest price a seller will take. As an investor if you do not mind mingling in this, ETFs are screaming for you.

Index funds couldn't care less. They play by the NAV (Net Asset Value) rules. The fund just waits for the market to close, tallies up the total value of its assets, and gives everyone the exact same fair and square price. Index funds are just the chilled bro.

Investment Minimums

The big money club is open, and who is sending out invitations? ETFs. ETFs just opened the velvet rope. ETFs are open and accessible since they trade like stocks, your minimum investment is usually just the price of a single share. With many brokers offering fractional shares, you can literally start with the spare change in your pocket. It's a low barrier, high freedom party where you receive a "come as you are" invitation.

Index Funds however can be a bit exclusive, They are checking IDs at the door. Many of the top-tier funds require an initial "buy-in" minimum, which can be a whopping hundreds to several thousand dollars. This may seem like a hurdle but it is actually a safety belt to keep the funds stable and attract serious, Long-term builders.

Cost Components

See yourself being invited to dinner where one is a prix-fixe menu with everything included and the other is a trendy à la carte spot where you pay for exactly what you order.

Index Funds are that all-inclusive dinner, you pay one clear expense ratio, and because you’re buying directly from the source, there are no hidden cover charges like commissions or market spreads. It’s the ultimate clean bill for investors who want a predictable experience. A straight one fee.

ETFs, meanwhile, are the à la carte stars, they often boast the lowest base "menu prices" (expense ratios) in the industry, but they come with small, live-market costs. Every time you "order" a share, you’re navigating the bid-ask spread and potential broker fees, which are tiny taxes on your transaction. If you're buying in bulk, the savings are massive, but for frequent small nibbles, those little extras can add up.

Tax Efficiency

Every investor is low-key obsessed with how much of their hard-earned gains the taxman is going to snatch away at the end of the year.

ETFs are the ultimate tax-dodging ninjas of the financial world thanks to their clever creation and redemption mechanism. Instead of selling stocks for cash (which triggers a tax bill), they swap them behind the scenes with big institutional players in a way that the IRS doesn't count as a "sale." This means you can sit back and watch your money grow without getting hit by random capital gains taxes just because the fund had to do some internal housekeeping. They are tax-shielded with sleek movement.

Index Funds, however, are a bit more old school and communal, sometimes to a fault. When other people decide to sell their shares, the fund manager often has to sell actual stocks to give them their cash, which creates capital gains that get distributed to everyone still left in the fund. You could be a loyal, long-term holder and still get stuck with a tax bill in the mail just because your fellow investors decided to cash out. It’s a bit like paying for a round of drinks you didn't even get to sip. Shared assets equals shared tax bills.

Automation and Investing Behavior

As investors, we are often our own portfolio’s worst enemy, and the vibe of your investment can either keep you disciplined or bait you into making a mistake.

Index Funds are the undisputed kings of the set it and forget it lifestyle, designed specifically for the chill investor who wants to automate their way to wealth. It removes the human element entirely. You aren't tempted to check the price or time of the market because the fund is built to just hum along in the background while you live your life.

ETFs come with a serious temptation to speed , just like having a sports car. Since they trade live like stocks, they give you the power to buy and sell at any second. which is great for control, but dangerous if you’re prone to panic-scrolling through financial news. They require more behavioral discipline.

Which Is Better for Different Investor Types?

Now we come to the big question, which is better? The truth is, there is no universal champion in this ring because the best choice is entirely about your personal financial frequency and behaviour.

Long-Term Automated Investors

Index funds are advantageous for investors who want to build a fortune without making it a full-time hobby. They are the undisputed soulmates of the set it and forget it crowd, letting you automate your contributions down to the penny.

Tactical Investors

ETFs are tactically flexible and offer the ultimate power user experience for investors who want to pull the strings in real-time. They are the perfect match for the cost-conscious optimizer who demands the lowest possible expense ratios and the freedom to dodge tax bills through those clever behind-the-scenes swaps. Do you have the discipline to stare down a live ticker without flinching, if yes, these are your high-performance tools for precision wealth building.

Beginners

For the fresh-faced investor, ETFs are the entry point because you can buy into the market for the price of a single lunch. They offer instant accessibility without the scary VIP-only minimums, though you'll need to resist the urge to play day-trader with your new toys. Index Funds are known for their safety net because they handle all the heavy lifting of automation while keeping you from making rookie emotional mistakes.

Retirement Investors

For retirement accounts, Index Funds let you schedule your savings and walk away for thirty years. Since these accounts are already tax-sheltered, you can ignore the fund's internal tax quirks and just focus on consistent, mindless growth.

Real-World Portfolio Use Cases

At this level, you already know the best choice stems from how you handle your money, your taxes, and your own impulses. Let’s look at these funds from a point where we all cannot get it wrong, examples.

Dollar-Cost Averaging Strategy

You being an investor who commits to investing $200 every Friday regardless of the market's mood. Index funds excel here because they allow you to buy in exact dollar amounts rather than full shares.

If the fund is trading at $300 per share, your $200 doesn't get rejected for being "not enough"; the system simply buys you 66% of a single share (0.66 shares).

Tactical Allocation Changes

Suppose a sudden economic shift occurs at 10:00 AM, and you decide to reduce your exposure to a specific sector immediately. With an ETF, you can execute a limit order to sell your position at a specific price right that second.

While an index fund investor must wait until the market closes at 4:00 PM to see what price they actually get, the ETF investor has already pivoted and moved their capital into a new position.

Core-Satellite Portfolio

Or are you an investor who wants the best of both worlds, the unshakeable foundation of an index fund and the high-growth potential of specific ETFs. In this strategy, you use a broad Index Fund as your Core, the heavy-lifting center of your portfolio that tracks the entire market (like the S&P 500). Then, you surround it with Satellite ETFs, smaller, specialized bets on specific sectors like Artificial Intelligence, Clean Energy, or Robotics.

Conclusion

The choice between an index fund and an ETF lies on whether you value hands-off automation or tactical precision. If you want a set-and-forget habit, choose the index fund, if you want rock-bottom costs and total control over every trade, the ETF is your winner.

You could still decide to invest in both, whichever you choose or even going for both, is still a win-win strategy.

Disclaimer: The content provided in this article is for educational and informational purposes only and should not be considered financial or investment advice. Interacting with blockchain, crypto assets, and Web3 applications involves risks, including the potential loss of funds. Venga encourages readers to conduct thorough research and understand the risks before engaging with any crypto assets or blockchain technologies. For more details, please refer to our terms of service.